In preparing for retirement, culture should be leveraged. The triggers and obstacles to retirement savings are different for Hispanics, Whites, and African-Americans. Culture helps and hurts. Learn to change their mindset, leverage their culture and prosper financially.

A one-size-fits-all financial education does not work in the real world. Changing a financial behavior is a challenge particular to a single person at a particular moment in time. Learn the financial skills that can improve your relations with money.

The average person is now responsible to figure out how much to save, where to invest it, consider risk, and make it last through a very long retirement lifespan. This is too much to ask from the average person. Plan for a retirement that makes sense for you.

Welcome To Retire Friday

The retirement models of the past will hardly work in the future.

Increased longevity, demographic growth and technology are all impacting the job market. New work models are based on just-in-time supply and demand of labor, hence the rise of the gig economy. Our jobs are being disrupted, and equally important, the labor arrangements that go along with them.

In this context we need to think differently about retirement. It is likely that you are going to live to be 100. Social Security will push retirement age to 70, so the first 20 -25 years will be preparing for independent life, working the next 40-50, and then resting for the next 30-40. This does not seem a balanced outline to us.

In the 40 to 50 years working life, sabbaticals, shorter workweeks, breaks in service and retraining will be likely. Even carrier changes and volunteering. Variable income will be more prevalent than salary and it will be our responsibility to manage the flexible nature of work to the steady demands of our financial needs.

30 to 40 years in retirement is a lot! We’ll need to change its outlook! A life of purpose, social connections, health and exercise will play a role. So will learning to balance our lifestyle to our future income, which depends on promises from the government, employers, and ourselves.

We’ll help you focus in what you can control and take ownership of your life, health, career and future, commit to live within your means, constantly increase your human capital, and prepare to Retire Friday.

Our Mission

Our Vision

Our Approach

We recognize that every person is at a different moment in their financial journey, their needs are unique, yet age cohorts follow certain spending patterns. We help our clients understand where they are and provide each individual with a sequence of learning outcomes that makes sense for them.

Our People

Our Services

Our Clients

Our Story

In order to research the discrepancies in wealth among races and the low participation of Hispanics in retirement programs and do something about it, we founded Hispanic Wealth in 2012. The problems we found were not exclusive of the Latino community, but they are present in lower-income earners of all ethnicities.

We came together as a team and founded Retire Friday to emphasize the need for shorter time horizons to help visualize retirement in these groups.

Our Founders

Manuel Carvallo

Chief Executive OfficerOur founder, Manuel Carvallo, is an actuary with over 30 years of retirement experience serving retirement programs, institutional investors and financial institutions. His experience includes consulting defined benefit and defined…

Our Beliefs

- You are likely to live a very long life…

- Retirement is either too far away or just too long…

- Your career will include periods of employment, self-employment, retraining, and time-in-between…

- Your job is threatened by either a person, a robot, automation, or artificial intelligence…

- Financial markets are complex and not in your control…

- And yet… you are accountable. Nobody cares about your retirement more than you do.

The why…

Our journey starts with a wake up call on racial equity.

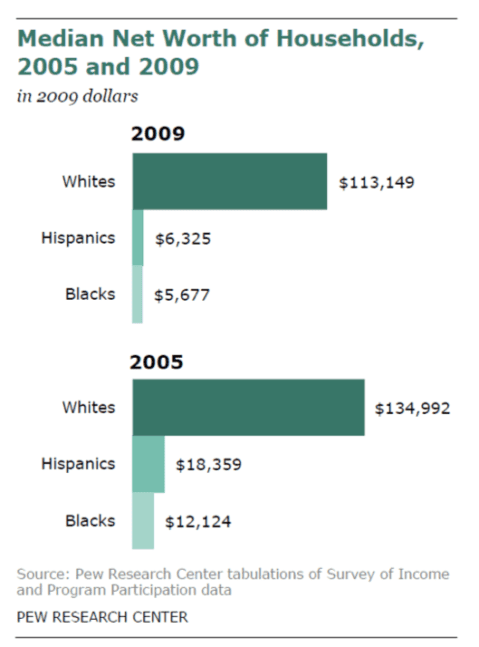

In a report published in 2011, the Pew Research Center got our attention with a report studying the wealth gaps between Whites, Blacks and Hispanics. Twenty-to-One it was called.

Worth noting is not only the big discrepancies in overall wealth of both Hispanics and Blacks when compared to Whites (5.6% and 5.0% respectively) but the impact the financial crisis had on their wealth. A loss of 66% and 53% for Hispanics and Blacks, while -16% for Whites.

Reasons can be traced not only to lack of financial education, but also to the fact that Blacks and Hispanics are targeted by abusive lenders and predatory practices.

The projected future

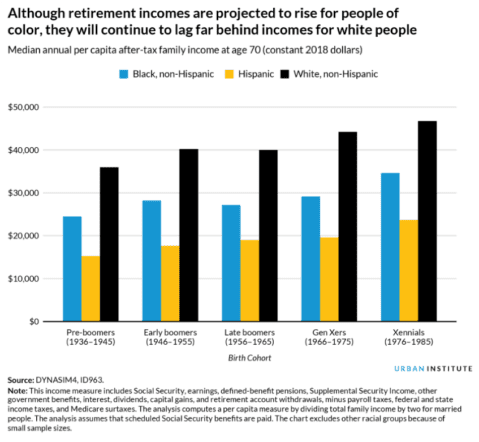

And then racial inequity is projected into the future...The Urban Institute warns us as part of their FEATURES reports Nine Charts about the Future of Retirement (July 23, 2019) of the continuation of this trend.

There will be not much to do then. No philanthropy will be enough to solve the massive scale of the problem then, but a little now, can alleviate the problem.

We don’t want to give them fish but teach them how to fish. And that is providing education.

Our Approach to Financial Literacy

We provide culturally-adequate educational videos with aims to increase the financial literacy of our clients. The video to the right is an example of how we explain “compound interest”.The example leverages the rural background of the target audience in explaining the incredible power of compound interest.

Characteristics of the education we provide…

- Visual and easy to understand

- Very well researched

- Free of conflicts of interest

- Adapted to culture

- Treats the person with respect

We created a series of videos as a test concept and were granted a 2019 Pensions & Investments Eddy Award.

A series of videos, all in Spanish with English subtitles, aimed to explain key concepts of the U.S. financial system to new Hispanic immigrants, with tutorials on how compound interest works, how to buy a car and obtain credit, among other topics. Judges praised the materials for their originality and use of relevant examples for the target audience.

We’d Love to Hear From You

5815 Windward Pkwy

Suite 302

Alpharetta, GA 30005